Cap Rate Calculator: How to turn $500k into $12.5M

Cap rate and other metrics to think about when looking at Real Estate

I recently purchased an apartment complex in Austin, Texas at a 4.24% Cap rate. One thing I’m going to do immediately on this property is to reduce the marketing budget by $10k per year. The property is in a prime location right off the highway, and therefore it gets organic traffic. By reducing the expenses on the property by $10k, the sales price of the property will increase by $236k! How could this happen you ask? Well, it’s all about understanding how to use Cap rates to your advantage. If you understand what a Cap rate is, you can turn $1M into $25M. In this blog post, I’ll show you how — among everything else you need to understand about Cap rates.

If you’re just here for the Cap rate Calculator, you can click here. But I suggest you read on if you really want to know how to use Cap rates to your advantage.

Why this Post, and How it’s Structured

There’s plenty of articles on “Cap rates” and “Cap rate calculators” but for some reason they’re either too simple or too complex. I wanted to write a post that really explains Cap rates deeply and make things as simple as possible — but no simpler.

“What’s the Cap rate?” is the most frequently asked question in Real Estate. And people ask this question mainly because they’re trying to understand the value of a certain piece of Real Estate. In reality, you must understand many other aspects when evaluating a Real Estate deal to understand if you are getting a good deal, but Cap rate is one good indicator. This blog post is the single-best resource you will ever read to understand what is a Cap rate, why it’s used, it’s benefits and drawbacks, other metrics to supplement Cap rate, and other questions to ask so you can be a better evaluator of Real Estate deals.

Here’s everything I’m going to cover. Feel free to jump around and make it a choose-your-own adventure based on your honest comfortability with understanding Cap rates.

- What’s a Cap rate?

- How to calculate Cap rate?

- Comparing Cap rates of Facebook vs. Real estate

- How to turn $500k into $12M

- The importance of the Exit Cap rate

- Comparing different Cap rates across the U.S.

- Limitations of Cap rate

- Who cares about Cap rates? Cash flow is king!

- Other metrics that matter besides Cap rate

- Conclusion

What’s a Cap rate?

A Cap rate, short for “capitalization rate” is one indication of the value of a property. It shows you the potential return that you can expect on a property if you were to buy a property with 100% cash. This is also known as the “unlevered return” because you’re not using leverage (Debt / Mortgage) to purchase a property.

The Cap rate is useful because it allows you to compare the unlevered return you can expect to receive on different investments. The Cap rate is also useful because it gives you an understanding of the value that you could sell your property for.

At a high-level, it’s pretty simple. Next, I’ll teach you how to calculate the Cap rate.

How is a Cap rate Calculated?

Cap rate is calculated by taking the Net Operating Income (NOI) of a property and dividing it by the proposed Sales price. This is known as the “going in Cap rate”, which takes the NOI from the last 12 months of the property and divides it by the sales price of a property. So for example, if I’m looking at an apartment complex that has generated $1M in NOI for the last 12 months and I have to pay $10M to buy the property, the Cap rate is 10% ($1M NOI / $10M Sales Price).

The sales price is easy to understand: it’s simply what you’re planning to buy the property for. But the NOI can be confusing at first, so let me explain how to calculate NOI. First, we have the Revenue of the property: this is all the rents that residents have paid for the last 12 months, as well as any additional income such as Admin fees, Utilities that residents pay for, late fees, etc. Next, you have your Operating Expenses (Opex). Opex is defined as all of the day-to-day expenses that are needed to run the property. These include things like payroll, repairs & maintenance, property taxes, marketing, and so on. A very important point — Opex does not include the mortgage payment So, Revenue minus Opex equals your NOI.

So, where does the mortgage payment (aka debt service costs) get reflected? Most people get a mortgage to buy Real Estate — after all, that’s the beauty of Real Estate: You can purchase a $10M property for only $3M. You gain leverage by only having to put down 20% - 30% cash and finance the rest of the deal with debt. The mortgage payments go “below the line”, which means it gets subtracted after NOI. So, you subtract your mortgage payments from NOI, which will equal your pre-tax cash flow.

The reason that Cap rate uses NOI as the denominator, instead of Cash flow, is because if you are a buyer who is planning to purchase the property you are going to have a different mortgage payment than the current owner. Your mortgage payment will be higher or lower based on the sales price of the property and the terms you are getting from your lender. So, the mortgage payments are not included in the Cap rate. This is very important to understand. If you only focus on the Cap rate you will fail to realize what your true return will be because you’re not calculating your cash-flow return, which includes your mortgage payments. And one of my favorite life principles is: Cash Flow is king!

We’ll talk more about Cash flow in the ‘Cash Flow is King’ section. But now let’s jump into the more exciting stuff - how to use Cap rates to compare investments and then how to make money by understanding Cap rates.

Comparing Cap rates of Facebook vs. Real Estate

The term Cap rate is primarily used in Real Estate, however you can use this same fundamental understanding not only to compare Cap rates across Real Estate deals, but compare any type of investment. I do these types of comparisons everyday when I’m looking at investments in different asset classes.

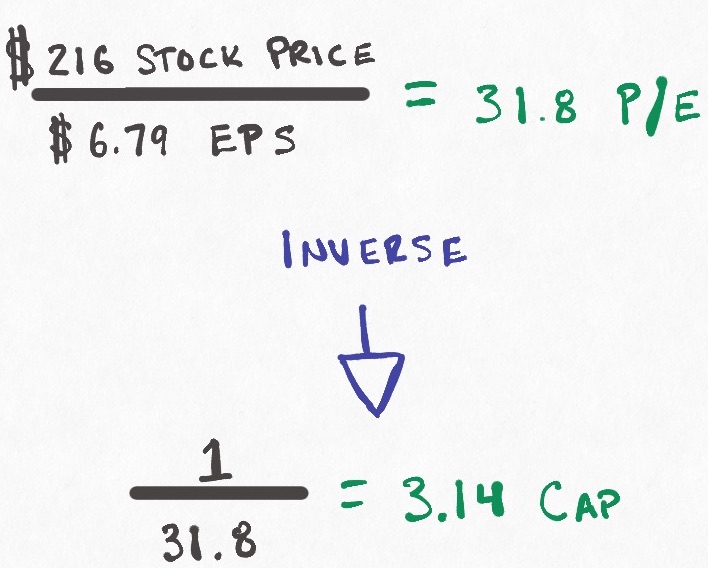

For example, investing in public equities, a similar metric is typically called Price-to-earnings ratio (P/E ratio). If you wanted to compare the value of investing in Facebook vs. investing in a Real Estate deal you may want to compare the Cap rates of each investment. First, you will start with the P/E ratio of Facebook — you would take Facebook’s current price to purchase a share and divide it by the last year of earnings to understand the P/E ratio. For example, Facebook’s P/E ratio as of this writing is 31.8. This is calculated by taking the $216 stock price divided by $6.79 earnings per share.

What you’ll notice is that when we calculate the Cap rate in Real Estate we’re calculating the earnings divided by the price, but in the Facebook example, we’re taking the price divided by the earnings. In order to have an apples-to-apples comparison, we need to take the inverse of the P/E ratio. We simply do that by dividing 1 over 31.8, which results in a 3.14% “Cap rate”. So if we compare our Real Estate deal above with a 4% Cap rate vs. the Facebook example of a 3.14% Cap rate, we can determine that we are getting a higher return on our Real Estate deal vs. purchasing Facebook.

This is a very simple way to compare investments, however there are two things two understand: First, there are different risk profiles with each of these investments which leads to varying Cap rates. For instance, which one is a bigger risk — investing in Facebook or the Real Estate deal you’re evaluating? It’s tough to say — you must do this analysis for yourself to understand the value that you are receiving relative to the price that you are paying.

Second, in Real Estate you can use leverage so you don’t need to pay 100% cash to buy a property — because of this, you get a higher return than the Cap rate since you are using debt to partially fund the purchase of your property.

In the next section, we’ll talk about one of the most overlooked aspects as it relates to Cap rates — how to use Cap rates to your advantage so you can multiply the return on your investment. This is crucial, and maybe the reason you’re reading this — because it will teach how you can can turn $500k into $12M by taking advantage of Cap rates.

How to turn $500k into $12M using Cap rates

Oftentimes, when people ask about Cap rates they are trying to understand the value they are receiving at the time of purchasing the deal. Sometimes when people hear of a Cap rate in the range of 4%, they get sticker shock because they think that they are paying too high a price. But all too often, people misunderstand how a Cap rate like this is advantageous to them as a buyer.

Let’s step back and think about this. I’ll use a deal that I am currently evaluating. I’m looking at another multifamily property in Austin, Texas and based on the current price it’s selling at a 4% Cap rate. The NOI for the last 12 months was $1M and the proposed sales price is $25M (4% Cap rate). Now let’s say I buy this and while I own the property I renovate some of the interiors, improve the condition of the property, make it a beautiful place to live, and manage it effectively. During that time, since I have invested money, time, and effort into the property and improved the condition, I will continually charge higher rents to live on the property because it’s a nicer place to live. Over time, because I was charging higher rents I might increase the income on the property from $1M to $1.5M.

Now, if I were to go sell the property and I can sell it at a 4% Cap rate, I am now going to sell the property for $37.5M ($1.5M NOI / 4% Cap rate). And that is the beauty of Real Estate! I bought the property for $25M and I added $500k in increased income — my property value did not just increase by $500k to $25.5M … but instead it increased by $12.5M to $37.5M!

What you may have noticed by now is that commercial Real Estate is primarily valued on a multiple of Net Operating Income of the property using the Cap rate. Because of this, in the example above we were able to increase the value of our property by 25x for each additional dollar we earned. This is why every dollar saved and earned on the property is so valuable. If I save an additional $1 in expense or generate an incremental $1 in revenue, I have increased the sales price of my property by $25. This is why it’s so important to differentiate CASH-FLOWING REAL ESTATE versus Real Estate that doesn’t Cash flow. Commercial Real Estate is valued based on the income it generates – your house is valued only based on what others think of the neighborhood.

The importance of the Exit Cap rate

In our examples, we’ve been focusing on the going-in Cap rates which use the prior 12 months to calculate the Cap rate. However, when evaluating a deal you also must understand what will the Cap rate be at the time you go to sell the property. This is known a the “Exit cap” or “Terminal cap”.

As I explained earlier, Cap rates fluctuate based on many factors such as the macroeconomy, the local market, the neighborhood, the condition of the property, and other factors. Cap rates a decade ago for multifamily apartment complexes in Austin were nearly 10% and now they are closer to 4% — this is because of a strong economy, great location, and lower risk has been proven in this asset class.

When evaluating an investment property, I like to be conservative. I believe one way this conservatism should also be reflected in your Exit cap. Even when you are in a market that you believe is primed for growth, you still want to have a higher Cap rate that you forecast at exit — with the standard being 10 basis points increase per year. For example, if I am buying a property at a 4% cap and I plan to sell the property in 5 years I may forecast an Exit cap of 4.5%.

Here’s an example to highlight just how important the Exit cap can be when determining the sale price of the property. Using our example above, we increased the NOI of our property to $1.5M and sold it at a 4% cap, which equaled a $37.5M sales price. Let’s say that instead of selling at a 4 cap, we had to sell at a 4.1 cap. This would result in a sales price decrease of $1M to $36.6M. This is how impactful the exit Cap rate can be — just a 10 basis point increase in Cap rates can swing your sales price by $1M.

Comparing different Cap rates across the U.S.

Cap rates differ across asset classes, cities, neighborhoods, where we are in the market cycle, and other factors. You cannot directly compare a 4% Cap rate in Austin to a 12% Cap rate in Detroit and think that the investment in Detroit is better because you are paying less for it. You must adjust these Cap rates to determine the risk you are taking on and the reward you can expect. Again, this is analysis you must do yourself to determine the risk-reward dynamic across different investments.

To give you a visual of how different Cap rates, can be you can look at the below map from CBRE from the 2nd half of 2019, which shows Cap rates across Multifamily in the U.S. You can see Cap rates vary from as low as 2% all the way up to over 12%. You can play around with this map here.

Limitations of Cap rate

There are many limitations to the Cap rate. When evaluating any Real Estate investment you must understand other metrics as well as the overall economic environment, business plan, market, and management team.

First, the going in Cap rate is only telling you the percentage return that you can expect if you were paying 100% cash, which we know never happens when buying Real Estate. Because the Cap rate does not calculate the true cash flow return that you will be receiving. You would determine this by calculating your cash-on-cash return, which we talked about earlier. Again, this is a very important point, because receiving a mortgage means you can reduce your initial investment by up to 80% and your cash-on-cash return could be 2-3x the Cap rate! We’ll talk about this more in the next section.

Second, the going in Cap rate does not tell you anything about how you can increase the income of the property. In order to understand that, you must look at the future projections and business plan to understand how the management team will increase the value of the property. You should also look at what are the comparable properties in the area doing. If you’re planning to raise rents from $1k to $1.2k but your competitors are currently only charging $1k then why is a resident going to live at your property? You must dig in on the business plan to make sure it makes sense.

Third, for many high net worth Real Estate investors, tax advantages are a huge benefit to investing in Real Estate. Although the Cap rate includes Property taxes in it’s calculation (Property taxes are part of Opex), it does not tell you anything about how you will be taxed on your cash flow distributions. Oftentimes in Real Estate the investor has the ability to reduce their taxable income substantially because of Real Estate accounting rules such as depreciation or 1031 exchanges. For example it’s not uncommon for a Real Estate investor to generate $1M in cash flow per year, but for purposes of taxes be able to recognize a $500,000 loss and therefore get a tax credit. You can read an example of how these depreciation tax benefits work if you click here.

Lastly, the Cap rate does not tell you anything about the risk profile of the deal. It is one indicator that will help you understand the potential value of the deal. But what if you believe the Cap rate is mis-priced? This can either mean you are getting a great deal — or it may mean you are overpaying for a deal. You must dig in to understand supply and demand in the market, the condition of the property and costs associated with upkeep, vacancy rates, operating expenses, and the ability of the team to execute their plan.

Now that you understand the limitations of Cap rates, let me tell you about Cash Flow!

Who cares about Cap rates? Cash Flow is King!

Now that we’ve talked in depth about Cap rates, you may notice that Cap rates do not give you the information you need to calculate your Cash-on-Cash return. This is important, because Cash-on-Cash is the true percentage return that you can expect to receive on your investment. Remember, the Cap rate is calculated by taking NOI divided by the Sales price. But this is not the correct calculation to determine our true return because in Real Estate you buy a property with only a portion of cash and the rest is financed by a mortgage. So, how do we calculate Cash-on-Cash return?

Simple: We take the Cash Flow forecast divided by our Equity Investment. Let’s use a real life example. I recently purchased a property for $35M in Florida. The prior 12 months NOI was $1.4M, which means my Cap rate was 4% ($1.4M NOI / $35M Purchase Price). In order to purchase the property, I needed to raise Equity (cash) of $10.5M from my investors, which was 30% of the total purchase price for the equity of the property. The other $24.5M (70% of purchase price) I needed was being provided from the lender, which is my mortgage. For my Financial forecast for the 1st year, I used the same Revenue, Opex, and NOI from the seller’s Profit & Loss Statement from the prior 12 months, which was $2.8M Revenue, $1.4M Opex, and $1.4M NOI. A side note here is that I’m being conservative because I’m not forecasting that I will increase income on the property, but rather have 0% year over year growth. Now, my mortgage payment for the first year is going to be $400k. I owe this to the lender in the 1st year for the $24.5M they provided me to purchase the property. To calculate my cash flow for year 1 I will take Revenue - Expenses - Mortgage Payment (Debt Service costs) = Cash Flow. This comes out to $1M in Cash Flow. In order to calculate my Cash-on-Cash return I will take the Cash Flow and divide it by the Equity (cash) my investors had to invest into the building, which was the $10.5M. This means my Cash-on-Cash return is almost 10% ($1M Cash Flow / $10.5M Equity Investment). Not bad.

Although Cap rates are important to deeply understand, they’re not going to give you a true picture of what your cash flow return is. This example shows that very clearly: We bought the property at a 4% Cap rate, but our Cash-on-Cash return is 2.5x our Cap rate! This is because of leverage. We create leverage by not needing to purchase the property with 100% cash. If we bought the property with 100% Cash, then our Cash-on-Cash return would be equal to the Cap rate of 4% because our initial investment would be $35M and our Cash Flow would be $1.4M since we have no mortgage payment. However, by decreasing our initial investment by 70% because we receive a mortgage from the property, we’re able to generate much greater returns.

As we head towards the final section, I’ll give you some more metrics that will be useful to evaluate the risk/reward profile of a property.

Other metrics that matter besides Cap rate

There’s other metrics to consider when evaluating a property besides the Cap rate. Here’s a few that come in helpful when evaluating an investment property.

- **Debt Service Coverage Ratio (DSCR) = Debt Service Costs / NOI ** … this ratio will help tell you how much leeway you have between the NOI that you generate and your mortgage payment. The lower the number, the less margin of safety you have to play with. For example, if your DSCR is 1 that means you’re only generating enough Income to cover your Mortgage payment — not a good position to be in.

- Cash on Cash Return = Annual cash flow / Down payment … how quickly you’re return is being generated. if you had $20k down payment and you made $20k in annual cash flow in 1 year your return is 100%; 2 years is 50%

- Gross income = everything including rent, laundry, vending machine, late fees, etc.

- Effective gross income = income - (vacancy % * income)

- Vacancy = unoccupied units

- Vacancy rate = number of vacancies / # of units

- Breakeven = total operating expenses + annual mortgage payment / gross potential income … this shows you what your break even point is. Essentially, what your vacancy rate can be before you lose money

Conclusion

Cap rates are one of many fundamental aspects to learn about understanding Real Estate. Often times it is misunderstood and people just ask about the Cap rate because they have heard people talk about it before. But you must understand what you’re trying to figure out by asking about the Cap rate — and I hope this guide has been good education for what you can understand, and more importantly, not understand by knowing the Cap rate. Once the Cap rate is understood, you can spend more time gathering information on everything else about the property such as the metrics I mentioned above, the business plan, the market, and the team before making a decision on if a property is the right investment for you.

Thanks to Adam Tank, Praveen Anuraj, Ike Mutabanna, Puja Talati, and Sapan Talati for reviewing drafts of this.